======================

What happened and why

1. Pakistan exchequer - Dollar peg suited them as it borrowed at lower dollar rates. It used the loans to create an unsustainable fiscal deficit, where prudence was abandoned. Eg. poor tax collection from the rich (ie. direct taxation), imprudent govt spending (incl. corruption), excessive & wasteful imports of capital goods from China (eg CPEC).

2. Elites and military - Low import prices and low taxation of the wealthy led to run-away imports of luxury goods & military equipment, and higher (illegal) capital outflows. Domestic investment was diverted to real estate, etc rather than productive investments.

3. Foreign contributions - For long, Pakistan received freebies, discounts, grants in kind, high remittances. Foreign partner countries cut back on this aid, partly due to financial or national compulsions, and partly due to Pakistani misadventures.

4. Artificial and unsustainable growth - Higher growth was fueled by borrowings & foreign contributions, and not due to domestic production.

5. Exports - Exports suffered, creating an imbalance in trade and a capital account deficit. This was compounded by FTA with China on Chinese terms and the systematic erosion of export competitiveness, eg by reneging on export incentives, electricity blackouts, water shortages, violence.

6. Foreign competition - Bangladesh, Vietnam, India, etc became more competitive through business-friendly reforms, infrastructure upgrades and human capital investments.

7. Nefarious activities - We can't be sure about the scale of Pakistan's illegal drugs trade, printing of foreign counterfeit money, terrorism paid for by wealthy countries, etc, -- on whether it remains a thriving business for Pakistan. But due to its nefarious activities, Pakistan has been put on the FATF's Grey list.

8. Machoism and isolation - While Pakistan sees itself as a macho country -- a first among equals--, others have worked patiently to bring it down to mother Earth. Its bravado and falsehoods were countered and despatched. It even lost friends and the little influence it had as a sovereign nation in the UN. Due to its machoism, Pakistan has become increasingly isolated from international trade and FDI.

Consequences

Pakistan needs to deal with the high inflation, high fiscal deficit, low direct taxation & high military spending, low exports, low foreign reserves, low remittances, low growth and rising poverty, etc. Also,

1. The loss of nominal GDP per capita is inevitable, as currency devaluation will far exceed domestic inflation plus growth.

2. Costly foreign borrowings and unwise CPEC investments (imprudent and bloated) will impact all concerned for years to come.

3. Lack of long-term planning & investment will cause shortages of water, etc, raise the cost of doing business (eg. high electricity prices) and lower growth of incomes.

4. Lack of human capital investment and high fertility rate will cause more misery for Pakistan and almost every other country.

5. Nefarious activities will weaken Pakistani sovereignty both internally and externally.

April 7th, 2019

Economic woes of Pakistan

=================

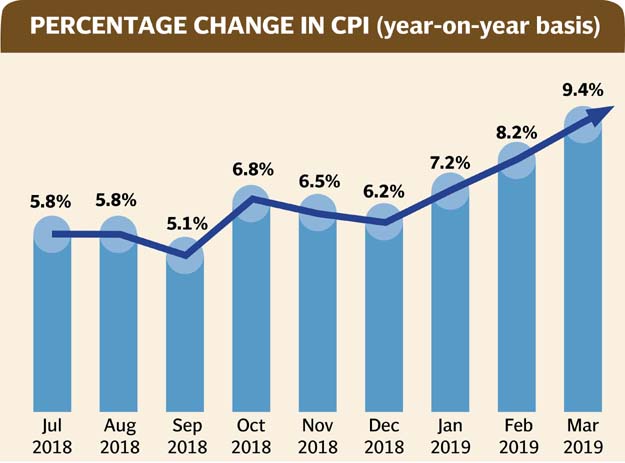

Inflation skyrocketed to a five-year high of 9.41% in March. The inflation rate has increased by 1.42% in March itself, over the last month. With inflation approaching double digits and economic growth rate slowing down to below 3%, the country is trapped in stagflation. Stagnation will worsen as Pakistan raises interest rates to overcome the surging inflation rate, which the International Monetary Fund (IMF) has predicted would hit 14%.

A noted Pakistan economist warns that Pakistan will see 4 million more people move into poverty and 1 million more people will be without jobs this year. Pasha says that due to high growth in working-age population (or labour force expansion), 1.8 m more people would come in the market but only 0.8 m people will find jobs. As a result, the unemployment rate would surge from 7.5% to 8% by June 2019.

Monetary policy response by Central bank

------------------------------------

The latest inflation data has affirmed the central bank’s apprehensions about persistent inflationary pressures (see below). It increased the key policy rate to 10.75% this week, which is close to the IMF's suggestion on interest rates. The IMF has long been advocating tight monetary and fiscal policies to cut the aggregate demand and restore macroeconomic stability. The central bank has cumulatively increased the interest rate by 5% since January last year. However, the positive gains of increased interest rates have been nullified by expansionary fiscal policies and devaluation of the currency.

Inflation score

-----------

The core inflation has stabilised at 8-8.5%, but the headline inflation has grown, due to rises in administered prices of electricity and gas, more costly perishable foods, and higher prices of imported goods.

Cost of living has shot up. The housing, water, electricity and gas group has increased by 11.6%. This group at 29.4%, has the second largest weighting in the inflation index. The perishable food sector has surged by 22% while the transport sector has increased by 13%.

Some of the goods have seen abnormal rises. In the year to March 2019, the tomato prices increased 315%, economy class train fares by 201.5%, green chillies prices by 151.7%, gas prices by 85.3% and bus fares by 48%.

The pulses have also surged massively. Similarly, English book prices have leapt up by one-third, MBA tuition fee by over 28%, CNG prices by 25.4% and cars by 24%. Cement became expensive by 14%, LPG cylinders by 13.5%, high-speed diesel by 13.1%, mutton by 12.4%, etc.

Inflation jumps to a five-year high of 9.41% in March,

Falling GDP growth, macroeconomic instability

=========================

Asian Development Bank paints a worrying picture of Pakistan’s economy, saying that economic growth will slow down to 3.9% and there will be higher inflation, a sizeable current account deficit and continued pressure on the exchange rate. It affirms the negative trend for at least two years.

♦ Deceleration of GDP to 3.9% in FY to June 2019 and 3.65% in FY 2019-20. Pakistan is falling behind other S Asian countries including Maldives and Nepal.

♦ Inflation will be at 7.5% by FY 2019. The rise is not only due to hikes in gas, electricity, customs duties and lagged impact of currency devaluation but also continued heavy government borrowing (or fiscal loosening).

♦ Current account deficit, which was 5% GDP or $14 billion in last fiscal year, will remain high -- though $ 5 billion lower than last fiscal year.

♦ Foreign Exchange reserves which had dropped to $8.1 billion in February 2019 (before lending support) will remain stressed in July 2019. There is minimal cushion in FEx to meet the elevated current account deficit in the next fiscal year (2019-2020), notwithstanding the lending support of $7.9 B, pledged by friendly countries (eg. China, Saudi & UAE) in early 2019.

♦ Public debt as % GDP will grow. It increased to 72.5% of GDP by June 2018 and is expected to continue in that vein.

♦ Macroeconomic weakness is signified by the twin deficits of unsustainable fiscal deficit & current account deficit. The bank predicts the government would miss its revised budget deficit target of 5.6% of GDP.

♦ Due to the economic slowdown, the country will be falling into worsening poverty and joblessness. Agriculture is under-performing on account of water shortages in the wet season. Large-scale manufacturing has contracted across the board at 1.5% overall, as domestic demand shrank, and rising imported prices hit manufacturing raw materials. In turn, low consumer demand has subdued the service sector.

♦ Higher interest rates and IMF will dampen growth in private consumption. Cuts in public-sector development funds will reduce investment and future growth prospects. However, lower and flexible currency values, higher import duties and dampened domestic demand will result in net exports and this will support GDP growth (to an extent).

♦ Government spending is growing unceasingly due to higher interest payments and defence spending, and revenue collection is far below expectations. On the other hand, the economic reform package in March 2019 mini-budget provides incentives to businesses for investments and exports and aims for reforms in Ease of doing business and export-orientated activities.

April 5th, 2019

April 5th, 2019

|

| Pakistan's Foreign Exchange Reserves become critical by end-2018 |

No comments:

Post a Comment